Medicare Supplement

What is Medicare Supplement?

A Medicare supplement (Medigap) insurance, sold by private companies, can help pay some of the health care costs that Original Medicare doesn’t cover, like copayments, coinsurance, and deductibles.

Some Medigap policies also offer coverage for services that Original Medicare doesn’t cover, like medical care when you travel outside the U.S. If you have Original Medicare and you buy a Medigap policy, Medicare will pay its share of the Medicare-approved amount for covered health care costs. Then your Medigap policy pays its share.

How Medicare works with other insurance

If you have Medicare and other health insurance or coverage, each type of coverage is called a “payer.” When there’s more than one payer, “coordination of benefits” rules decide which one pays first. The “primary payer” pays what it owes on your bills first, and then sends the rest to the “secondary payer” to pay. In some cases, there may also be a third payer.

What it means to pay primary/secondary

The insurance that pays first (primary payer) pays up to the limits of its coverage.

The one that pays second (secondary payer) only pays if there are costs the primary insurer didn’t cover.

The secondary payer (which may be Medicare) may not pay all the uncovered costs.

If your employer insurance is the secondary payer, you may need to enroll in Medicare Part B before your insurance will pay.

Paying “first” means paying the whole bill up to the limits of the coverage. It doesn’t always mean the primary payer pays first in time. If the insurance company doesn’t pay the claim promptly (usually within 120 days), your doctor or other provider may bill Medicare. Medicare may make a conditional payment to pay the bill, and then later recover any payments the primary payer should’ve made.

If you have questions about who pays first, or if your insurance changes, call the Benefits Coordination & Recovery Center (BCRC) at 1-855-798-2627. TTY users should call 1-855-797-2627.

Note

Tell your doctor and other health care providers if you have coverage in addition to Medicare. This will help them send your bills to the correct payer to avoid delays.

What’s a conditional payment?

A conditional payment is a payment Medicare makes for services another payer may be responsible for. Medicare makes this conditional payment so you won’t have to use your own money to pay the bill. The payment is “conditional” because it must be repaid to Medicare when a settlement, judgment, award, or other payment is made.

If Medicare makes a conditional payment for an item or service, and you get a settlement, judgment, award, or other payment for that item or service from an insurance company later, the conditional payment must be repaid to Medicare. You’re responsible for making sure Medicare gets repaid for the conditional payment.

How Medicare recovers conditional payments

If Medicare makes a conditional payment, you or your representative should call the Benefits Coordination & Recovery Center (BCRC) at 1-855-798-2627. TTY users should call 1-855-797-2627. The BCRC will work on your case, using the information you or your representative gives the center to see that Medicare gets repaid for the conditional payments.

The BCRC will gather information about any conditional payments Medicare made related to your pending settlement, judgment, award, or other payment. Once a settlement, judgment, award, or other payment is final, you or your representative should call the BCRC. The BCRC will get the final repayment amount (if any) on your case and issue a letter requesting repayment.

Retiree Insurance

If you’re retired and have Medicare and group health plan (retiree) coverage from a former employer, generally, Medicare pays for your health care bills first and your group health plan coverage pays second.

The way your retiree group health plan coverage works depends on the terms of your specific plan. Your employer or union, or your spouse’s employer or union, might not offer any health coverage after you retire. If you can get group health plan coverage after you retire, it might have different rules, and might not work the same way with Medicare.

Five Things You Should Learn About Retiree Coverage

1) Find out if you can continue your employer coverage after you retire. Generally, when you have retiree coverage from an employer or union, they control this coverage. Employers aren’t required to provide retiree coverage, and they can change benefits or premiums, or even cancel coverage.

2) Find out the price and benefits of the retiree coverage, including whether it includes coverage for your spouse. Your employer or union may offer retiree coverage for you and/or your spouse that limits how much it will pay. It might only provide “stop loss” coverage, which starts paying your out-of-pocket costs only when the costs reach a maximum amount.

3) Find out what happens to your retiree coverage when you’re eligible for Medicare. For example, retiree coverage might not pay your medical costs during any period in which you were eligible for Medicare but didn’t sign up for it. When you become eligible for Medicare, you may need to enroll in both Medicare Part A and Part B to get full benefits from your retiree coverage.

4) Find out what effect your continued coverage as a retiree will have on both your health coverage and your spouse’s health coverage. If you’re not sure how your retiree coverage works with Medicare, get a copy of your plan’s benefit booklet, or look at the summary plan description provided by your employer or union. You can also call your employer’s benefits administrator and ask him or her how the plan pays when you have Medicare. You may want to talk to your State Health Insurance Assistance Program (SHIP) for advice about whether to buy a Medicare Supplement Insurance (Medigap) policy.

If your former employer goes bankrupt or out of business, Federal COBRA rules may protect you if any other company within the same corporate organization still offers a group health plan to its employees. That plan is required to offer you COBRA continuation coverage. If you can’t get COBRA continuation coverage, you may have the right to buy a Medigap policy even if you’re no longer in your Medigap open enrollment period.

Since Medicare pays first after you retire, your retiree coverage is likely to be similar to coverage under Medicare Supplement Insurance (Medigap). Retiree coverage isn’t the same thing as a Medigap policy but, like a Medigap policy, it usually offers benefits that fill in some of Medicare’s gaps in coverage—such as coinsurance and deductibles. Sometimes retiree coverage includes extra benefits, like coverage for extra days in the hospital.

When can I buy a Medicare supplement?

Buy a Policy When You Are First Eligible

The best time to buy a Medigap policy is during your 6-month Medigap open enrollment period, because you can buy any Medigap policy sold in your state, even if you have health problems. This period automatically starts the month you're 65 and enrolled in Medicare Part B, and once it’s over, you can’t get it again.

During Open Enrollment

Medigap insurance companies are generally allowed to use medical underwriting to decide whether to accept your application and how much to charge you for the Medigap policy. However, if you apply during your Medigap open enrollment period, you can buy any Medigap policy the company sells, even if you have health problems, for the same price as people with good health.

Find your situation below:

I’m 65 or older.

Your Medigap open enrollment period begins when you enroll in Part B and can’t be changed or repeated. In most cases, it makes sense to enroll in Part B when you’re first eligible, because you might otherwise have to pay a Part B late enrollment penalty.

I’m turning 65.

The best time to buy a Medigap policy is during the 6-month period that begins on the first day of the month in which you’re 65 or older and enrolled in Part B. For example, if you turn 65 and are enrolled in Part B in June, the best time for you to buy a Medigap policy is at some point between June and November.

After this enrollment period, your option to buy a Medigap policy may be limited and it may cost more. Some states have additional open enrollment periods.

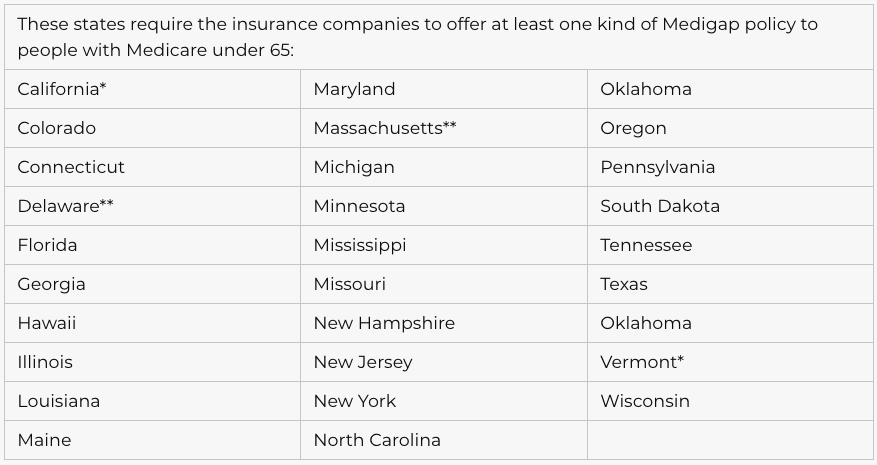

I’m under 65.

Federal law doesn’t require insurance companies to sell Medigap policies to people under 65. If you’re under 65, you might not be able to buy the Medigap policy you want, or any Medigap policy, until you turn 65. However, some states require Medigap insurance companies to sell you a Medigap policy, even if you’re under 65.

I have group health coverage through an employer or union.

If you have group health coverage through an employer or union because either you or your spouse is currently working, you may want to wait to enroll in Part B. Employer plans often provide coverage similar to Medigap, so you don’t need a Medigap policy.

When your employer coverage ends, you’ll get a chance to enroll in Part B without a late enrollment penalty which means your Medigap open enrollment period will start when you’re ready to take advantage of it. If you enrolled in Part B while you still had the employer coverage, your Medigap open enrollment period would start, and unless you bought a Medigap policy before you needed it, you would miss your open enrollment period entirely.

Outside Open Enrollment

If you apply for Medigap coverage after your open enrollment period, there’s no guarantee that an insurance company will sell you a Medigap policy if you don’t meet the medical underwriting requirements, unless you’re eligible due to one of the situations below.

In some states, you may be able to buy another type of Medigap policy called Medicare SELECT. If you buy a Medigap SELECT policy, you have rights to change your mind within 12 months and switch to a standard Medigap policy.

Find your situation below:

I’m under 65 and am eligible for Medicare because of a disability or End-Stage Renal Disease (ESRD).

If you have ESRD, you may not be able to buy the Medigap policy you want, or any Medigap policy, until you turn 65. Federal law doesn’t require insurance companies to sell Medigap policies to people under 65.

* A Medigap policy isn’t available to people with ESRD under 65.

** A Medigap policy is only available to people with ESRD.

If you’re already enrolled in Medicare Part B, you’ll be in a Medigap open enrollment period when you turn 65. You’ll probably have a wider choice of Medigap policies and be able to get a lower premium at that time.

Even if you don’t live in any of the above listed states, some insurance companies may voluntarily sell Medigap policies to people under 65, although they will probably cost more than Medigap policies sold to people over 65, and they can use medical underwriting. Check with your state about what rights you may have under state law.

For state requirements, call your State Health Insurance Assistance Program (SHIP).

If you have health problems.

During the Medigap open enrollment period, an insurance company can’t use medical underwriting. This means the company can’t do any of these things because of your health problems:

- Charge you more than normal for a Medigap policy

- Refuse to sell you any Medigap policy it sells

- Make you wait for coverage to start (except as explained below)

In some cases, an insurance company must sell you a Medigap policy, even if you have health problems. You’re guaranteed the right to buy a Medigap policy:

When you’re in your Medigap open enrollment period

If you have a guaranteed issue right

You may also buy a Medigap policy at other times, but the insurance company can deny you a Medigap policy based on your health.

I have a pre-existing condition.

The insurance company can’t make you wait for your coverage to start, but it may be able to make you wait for coverage if you have a pre-existing condition.

In some cases, the Medigap insurance company can refuse to cover your out-of-pocket costs for these pre-existing health problems for up to 6 months (called the “pre-existing condition waiting period”). After these 6 months, the Medigap policy will cover your pre-existing condition.

Coverage for the pre-existing condition can be excluded if the condition was treated or diagnosed within 6 months before the coverage starts under the Medigap policy. After this 6-month period, the Medigap policy will cover the condition that was excluded.

When you get Medicare-covered services, Original Medicare will still cover the condition, even if the Medigap policy won’t cover your out-of-pocket costs, but you’re responsible for the coinsurance or copayment.

Get more information on the Pre-Existing Condition Insurance Plan.

I have a pre-existing condition and am replacing “creditable coverage.”

If you have a pre-existing condition and buy a Medigap policy during your Medigap open enrollment period, and are replacing certain kinds of health insurance that counts as “Creditable coverage (Medigap),” it’s possible to avoid or shorten waiting periods for pre-existing conditions.

If you have had at least 6 months of continuous prior creditable coverage, the Medigap insurance company can’t make you wait before it covers your pre-existing condition. There are many types of health care coverage that count as creditable coverage for Medigap policies, but they will only count if you didn’t have a break in coverage for more than 63 days.

Get more information on the Pre-Existing Condition Insurance Plan.

I have other insurance.

If you have group health insurance through an employer or union, your Medigap open enrollment period will start when you sign up for Part B.

I have a guaranteed issue right.

If you buy a Medigap policy when you have a guaranteed issue right(also called “Medigap protections”), the insurance company can’t use a pre-existing condition waiting period.

How to compare Medicare supplement policies

Find out which insurance companies sell Medigap policies in your area.

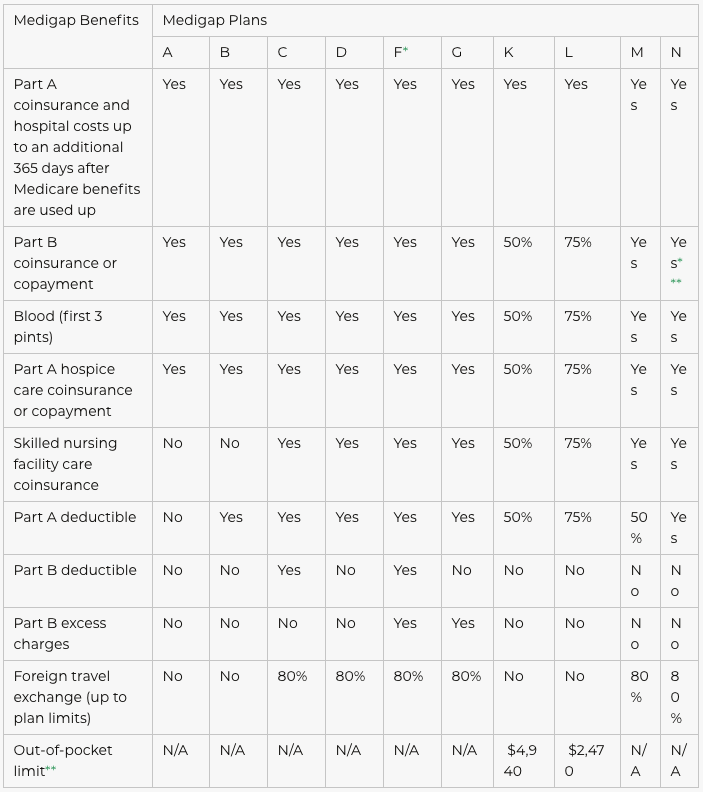

Medigap policies are standardized

Every Medigap policy must follow federal and state laws designed to protect you, and it must be clearly identified as “Medicare Supplement Insurance.” Insurance companies can sell you only a “standardized” policy identified in most states by letters.

All policies offer the same basic benefits but some offer additional benefits, so you can choose which one meets your needs. In Massachusetts, Minnesota, and Wisconsin, Medigap policies are standardized in a different way.

Each insurance company decides which Medigap policies it wants to sell, although state laws might affect which ones they offer. Insurance companies that sell Medigap policies:

Don’t have to offer every Medigap plan

Must offer Medigap Plan A if they offer any Medigap policy

Must also offer Plan C or Plan F if they offer any plan

Medigap Plans

Note

The Medigap policy covers coinsurance only after you’ve paid the deductible (unless the Medigap policy also pays the deductible).

Compare Medigap plans side-by-side

The chart below shows basic information about the different benefits Medigap policies cover.

Yes = the plan covers 100% of this benefit

No = the policy doesn’t cover that benefit

% = the plan covers that percentage of this benefit

N/A = not applicable

* Plan F also offers a high-deductible plan. If you choose this option, this means you must pay for Medicare-covered costs up to the deductible amount of $2,140 in 2014 ($2,180 in 2015) before your Medigap plan pays anything.

** After you meet your out-of-pocket yearly limit and your yearly Part B deductible, the Medigap plan pays 100% of covered services for the rest of the calendar year.

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in inpatient admission.

What is Medicare Supplement

Your Medigap policy may offer additional coverage for health care services or supplies that you get outside the U.S.

Standard Medigap Plans C, D, F, G, M, and N provide foreign travel emergency health care coverage when you travel outside the U.S.

Plans E, H, I, and J are no longer for sale, but if you bought one of these plans before June 1, 2010 you may keep it. All of these plans also provide foreign travel emergency health care coverage when you travel outside the U.S.

Medigap coverage outside the U.S.

Medigap Plans C, D, E, F, G, H, I, J, M, and N pay 80% of the billed charges for certain medically necessary emergency care outside the U.S. after you meet a $250 deductible for the year. These Medigap policies cover foreign travel emergency care if it begins during the first 60 days of your trip, and if Medicare doesn’t otherwise cover the care.

Foreign travel emergency coverage with Medigap policies has a lifetime limit of $50,000.

Find out before you go

Before you travel outside the U.S., talk with your Medigap plan or insurance agent to get more information about your Medigap coverage while traveling.